The Week That Was (3rd - 9th October, 2021)

The Week That Was (3rd - 9th October, 2021)

"Do not trade every day of every year." Jesse Livermore

“Do not trade every day of every year.” Jesse Livermore

Why hasn’t a movie about Jesse Livermore, the famous stock trader of the 1920s, been made btw?

It seems like the perfect time for one to be released. DiCaprio should play the lead. He just needs spectacles and fake ears. Jesse’s life was very similar to the life of the fictional Great Gatsby.

Jesse Livermore was a loquacious chap, by all accounts.

And his comment, stated above, about trading, was very relevant for this week.

You could easily have over-traded. There was just so much noise! It probably paid to sit on your hands.

The Debt Ceiling Must Go

The week was also a bit tedious, to be fair.

If we park the inflation discussion for one moment, the general theme has been repeated seemingly at this time of year, for as long as I can remember.

The pantomime around the debt ceiling is a waste of time and energy. We kind of know how it will end. Let’s stop the charade and just get rid of it.

The Fed should do nothing

Data points were few and far between but the key one, the jobs report, came out on Friday.

Unfortunately, there was something in it for the bulls and the bears.

With such inconclusive data, why do we think the Fed needs to do anything different?

Job creation appears to be behind the curve and there’s every reason to believe that a lot of the inflation we are seeing is due to temporary structural issues.

Jerome Powell is not getting on Time Magazine any time soon but if he tightens too early, and the economic recovery falters, he might as well move to Easter Island.

The Fed knows the BOJ and the ECB both messed up recoveries by tightening too early in the past. The Fed, itself, made the same mistake at the end of 2018. This is the time to be prudent and watchful.

And why would the Fed mess up all the good work they’ve done since Covid because Mohammed El Erian is pushing the stagflation narrative this month?

He needs to stop btw.

Queen’s College, Cambridge needs him to focus on ceremonial duties surely!

Stagflation: Another nonsense prediction

In 2009, we were supposed to worry about hyperinflation, remember?

I’m still waiting for that to happen.

Peter Schiff told us to buy gold, remember?

How’s that trade working vs the S+P?

Why hasn’t the US dollar collapsed, Peter?

Now we are told stagflation is around the corner.

Very credentialed people spin out sound bites on linkedin without, it seems, any thinking being done.

It’s amazing to me.

Inflation has picked up. That’s correct.

A lot of that is clearly due to Covid-related temporary structural issues.

Of course, there are serious problems in industries like chip manufacturing.

And these might take a while to sort out.

But stagflation occurs when inflation is out of control and growth is more or less zero. And that’s just not the case right now!

The US is growing at 6% and Europe is growing at 5% and the signs are the growth next year will be above trend!

This is not even close to the situation in the 1970s.

History might not be a good guide anymore

We might need to rethink our views on many things with interest rates so low. With the discount rate at these levels, do the normal valuation benchmarks apply, for example?

But it’s the comparisons with the 1970s that are just plain stupid.

Microsoft was just starting in the 1970s for one thing. Tech has had a massive deflationary impact on prices.

And Russ Roberts makes a great point about qualitative changes that have occurred since Abba and Sonny and Cher were in the charts. Watch it here:

It’s much more complicated than the pundits say it is.

Turning Japanese would be a bad thing

It surprises me that pundits don’t pay more attention to Japan’s economic history on CNBC.

Its example is particularly instructive because it is so recent. And it is so relevant to what Biden/Yellen/Powell are trying to do.

Japan went through deflation in the 1990s and 2000s.

It only shrugged it off with Abe’s 3 Arrows policy, announced in 2012.

There were three arrows:

Easy monetary policy.

Infrastructure spending.

Structural reform.

Sound familiar?

The three were needed to be done in tandem to jolt the economy out of deflation.

Loose monetary policy had not worked by itself.

Interestingly, Japan had debt that was equivalent to 200% of GDP in 2010. And Japan’s currency, the Yen, was actually quite strong.

Surely that fact would be an interesting point to be made on CNBC?

Abe was criticized for his stance but deflation did end.

And the economy managed an average growth rate of 1.1% between 2013 and 2020.

That’s obviously not great but it was better than it was before.

And the reason the policy wasn’t more effective was because Abe couldn’t get the needed structural reforms through the quagmire of Japan’s Diet.

It’s imperative that it’s all done in tandem.

Japan was dead for 20 years.

This cannot happen to the USA.

The domestic economy is just too important for the world. Japan’s domestic economy wasn’t.

Biden’s 3 Arrows

The BOJ, ECB and the Fed talk ALL the time.

They know a combination of easy money, huge infrastructure spend and structural reform is needed to jump start the economy out of the deflation trap. And they all worry about deflation more than inflation.

And that’s why Biden’s infrastructure and reform plan is so important.

To be fair, Biden did it again.

He delivered a speech that was magic!

I really didn’t know he had it in him. (I actually quite liked Trump!)

If Biden’s UN speech was similar to Kennedy’s Peace Speech in 1963, this speech was similar to Johnson’s Great Society Speech in 1964.

Listen to the reform agenda in particular. The child tax credits, for example, make so much sense!

“We are all Keynesians now” - Milton Friedman, Dec 31, 1965

Apparently, Friedman said this tongue in cheek but it’s a good quote, nonetheless.

It’s hard to exaggerate how significant what’s happening is.

It’s a decisive move away from the religion of Milton Friedman.

Education and infrastructure are being discussed as investments! That’s huge!

John Maynard Keynes has been in exile for a very long time.

He’s making a comeback and that is a good thing.

For the record, Keynes was no socialist and definitely not a Marxist. He was a realist. He knew sometimes economies needed help only government could provide.

I have started reading his works btw.

If you have time, read Economic Possibilities For Our Grandchildren and tell me you are not impressed.

He deserves a movie too btw. Tom Hanks?

“All I want to know is where I am going to die and not go there.” Charlie Munger

Charlie Munger loves inversion theory. He uses it to make investment decisions.

It’s not his theory, of course.

It belonged to the German mathematician, Carl Jacobi.

He solved difficult problems by following a simple strategy:

“man muss immer umkehren.”

“invert, always invert”

(The German is for my two readers in Germany. Vielen Dank!).

It’s possible we might be on the verge of a MASSIVE boom, the kind we saw from 1958-1967 in the US.

But that won’t be achieved without dramatic structural reform and a heavy amount of government involvement, similar to what Eisenhower started in the late 1950s. Eisenhower was a Republican btw.

Unfortunately, we have become entrenched in very narrow way of thinking based on arbitrary party lines that have been calcified over the last 40 years. It’s a problem everywhere in the Western world.

Keynes is not that familiar to us, for example, despite being a giant in the first half of the 20th Century. He was deliberately discredited by the Chicago school of economics.

We need to test our assumptions and our understanding of economic history as this is a critical moment for the world.

If we get it right, we will have a booming stock market, perhaps as impressive as the stock market during the Jazz Age of the 1920s. With so many great cash flowing tech companies, it should be a lot healthier market too.

Common Misconceptions Are Holding Us Back

We need to move away from common misconceptions/biases/set beliefs that don’t serve us.

Here’s my top 4 (there are many more):

The Fed is inherently evil

In 1991, only Ron Paul and, maybe Ross Perot, talked about the Fed in a critical way. Most people didn’t even think about it.

Alan Greenspan was even on Time Magazine in the 1990s. For many years, he was considered to have the midas touch.

In 2021, it’s a different ball game. Even high school kids know about the famous meeting on Jekyll Island.

It’s definitely funky to have a private bank (unaudited) with such incredible power in the economy but its role in the economy is not going away.

Its work after Covid was actually magnificent. That was our generation’s Second World War.

If the Fed hadn’t intervened, things would have got UGLY!

Let’s give the Fed a break.

(If you want to go down a rabbit hole, focus on the Ghislaine Maxwell case. That stuff is crazy and scary).

Janet Yellen is a megalomaniac

We seem to be so willing to take on board what your average narcissistic tech entrepreneur pays lip service to but give people like Janet Yellen no benefit of the doubt.

Incidentally, can we finally now put Sheryl Sandberg in the “very dangerous for society” category? “Leaning in” to her should come with a health warning.

Yellen has committed her life to studying labor economics. Her husband is an economist too. Their pillow talk is probably efficient wage thesis, not world domination.

Her net worth is $20mn. That’s decent but nothing compared to Tony Blair, Bill Clinton or Barak Obama.

She could have played the game very differently if she was driven by selfish motivations only.

We live in a cynical age but the concept of noblesse oblige still exists in some circles.

My view is she is the right person for the job right now.

And she’s a whole lot more impressive than Greenspan, who apparently was a bit like Tigger from Winnie the Poo: he desperately wanted to be liked, especially by investment bankers like Sandy Weill.

I think he could be a good Tigger actually.

Governments should be run like a household

The folksy approach to government was popular with Ronald Reagan but it got a lot of air play both sides of the Atlantic, to be fair.

Maggie Thatcher, with her handbag and her permed hair, loved pushing the “household fallacy” to middle class voters as far back as the 1950s as she played up the housewife image. It was lost on people how fabulously wealthy her husband was.

The simplicity of balancing books is appealing but it just doesn’t work when it comes to government, especially when there has been a shock. Austerity arguably nearly broke the UK over the last 10 years, did it not?

A household does not have to invest in jobs, pay for the sick and maintain infrastructure like governments do.

Even Ayn Rand groupie, Alan Greenspan, notes in his book, “The Map and the Territory: Risk, Human Nature, and the Future of Forecasting:”

“I have come around to the view that there is something more systematic about the way people behave irrationally, especially during periods of economic stress, than I had previously contemplated.”

(Yes, that’s the title of the book btw. Perhaps he is completely shut off from the real world).

Confidence amongst consumers is an incredibly important dynamic. It was absent in Japan in the 1990s and the economy sucked.

Consumers in the US must feel confident. They are crucial to world growth.

Inflation is always bad

If inflation is fire, deflation is ice.

Deflation freezes consumer spending as people wait for prices to fall.

Inflation actually boosts economic activity as people buy at today’s prices so they won't have to pay more later.

It can be a very good sign the economy is growing.

This is all seems self-evident but it’s important to repeat this as there is much misleading information on TV shows.

Deflation makes the rich hoard their cash. Look at Japan.

Inflation can help the indebted, the risk taker and the bold and the beautiful.

And there are a lot of beautiful risk takers in the US.

We need to create the right environment for them. That will involve the government, as it always has, really.

Other Tidbits:

Lagging Markets (China and Japan)

My opinion is equities still go higher, especially as interest rates are still low (they will be low for a very long time) and corporate earnings are so good.

If you can look beyond the US, both China and Japan are noteworthy laggards.

I bought Alibaba the other week. Charlie Munger seems to like it too. I think it’s rare to see a large cap stock like Alibaba at these valuations in what is a global bull market. My guess is one lucky broker got a 100 million dollar buy order from a value account in the US last week. It would tick so many boxes for fund managers with big funds to allocate.

Of course, if you don’t like single stock risk, check out the KWEB chart.

Separately, another stock that would tick boxes in Boston would be Sony in Japan. I think it leads the index higher.

There’s so many interesting stocks in Japan at the moment, actually. I think we will see Cathie Woods, for example, get more Japanese robotic firms into her portfolio soon. More on that in a future newsletter.

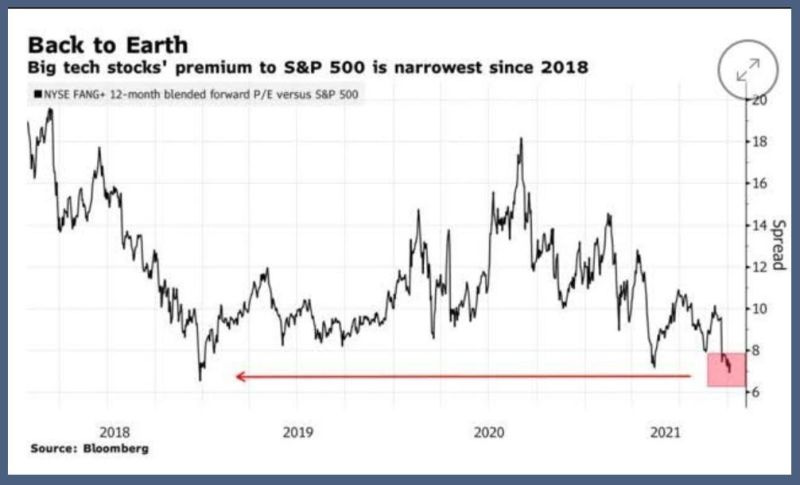

Tech Compounders Are The New Gold

When Whatsapp went down this week, I was a bit lost. I use it to call clients overseas.

FAANG stocks permeate through our lives more than Exonn did in the 2000s and Kodak did in the Nifty 50 era.

For me, stocks like Apple and Microsoft should be in everyone’s pension accounts.

My guess is Facebook will weather this storm. There’s no need to rush in but it should consolidate around $300-330 level.

I won’t buy it on principle. I will take Tim Cooke over Mark Zuckerberg any day of the week! (I’ll wait for the abuse after making this comment)

Cathie Woods - the King/Queen of Trolls

Cathie is amazing. And I just loved what she said last week:

“Today, $TSLA announced that in the third quarter it sold 241,300 vehicles globally, up 73% year on year (YoY) and 20% quarter over quarter (QOQ). Meanwhile $ GM blamed the 33% YoY decline in its US sales on chip shortages. What? # EVs require 3-5x more chips per car produced.”

How many companies will hide behind supply issues this earnings season? Time will tell.

As always, thanks for reading. If you like what you read, please share it with friends, colleagues and family. I am still in the building phase. Unfortunately, I have made zero progress on the design front. That’s coming. But I really have no patience with it or creative ability, to be honest.

Best regards

Mateen

DISCLAIMER: None of this is financial advice. The opinions expressed are purely my own opinions and it is imperative for you to do your own research. They do not represent the views of any company I am associated with.