The Week That Was (31st October-6th November, 2021)

The Week That Was (31st October-6th November, 2021)

"Man is born free, and everywhere, he is in chains" Jean-Jacques Rousseau

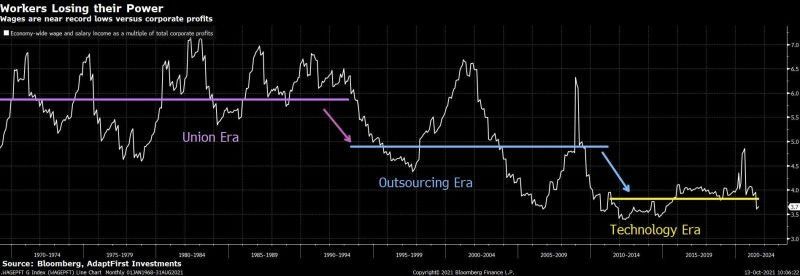

Social mobility is a religion in the US.

The idea that everyone is entitled to "life, liberty and the pursuit of happiness" has shaped American culture.

It’s what makes the country dynamic and special.

Surveys, conducted over the last 20 years, showed low wage US workers continued to remain optimistic about their chances to get ahead, despite falling further and further behind economically.

Something changed with Covid.

People decided they didn’t want their “shitty” jobs back.

Whether it’s coal miners in Alabama, Hollywood crew unions or health care workers in Buffalo, the US hasn’t seen this level of industrial dispute since the 1970s.

It’s not on the same level as Thatcher’s Britain but it’s hard to put the genie back in the bottle sometimes.

The stand out strike has to be John Deere.

The workers rejected the contract pay offer of effectively +23% for the first year and +5% for the second year.

This kind of thing is disruptive but it’s not necessarily a bad thing.

Things have obviously got way out of whack since the 1980s.

Paying workers a fair wage can have a wonderful multiplier effect for economies and businesses.

That was well known in the US for most of the 20th Century. Henry Ford was a big advocate, for example.

Wealth welling up on one side is bad for total wealth and productivity.

Capitalism is different from corporatism.

The US can’t look like Hong Kong.

The big question for investors is how to avoid the risks associated with increased industrial disputes.

For me, you don’t want to own any business that has low wage workers that doesn’t have pricing power on the other side.

Amazon and Walmart will do ok.

Second tier retailers may not.

That sort of thing.

Luxury stocks have pricing power and should be relatively safe.

I can’t imagine Ferrari’s stock price slowing down because of a strike.

High margin businesses like SaaS names and tech compounders should be fine.

When does Jerome Powell get his picture on Time Magazine?

In 1950, when the North Koreans fired the first bullets across the border into South Korea, the American public panicked.

They had lived through rationing only a few years before and knew what it meant to go without.

Mums, being Mums, raided the shops and fought over household necessities for their families.

Where have I seen that before?

History rhymes?

Given the increase in aggregate demand, CPI went higher.

It made the recent increase in 2021 look tame.

The Fed became independent of the Treasury in 1951. It seized upon the opportunity and said the rising CPI was a serious problem.

But before you could spell the word “inflation” out loud, the bond market had started indicating the problems would soon pass.

And within a few months, CPI started falling.

The FED got it wrong.

It was a temporary blip.

The bond market called it correctly.

This wasn’t the first time the Fed was too hawkish about inflation. It had done the same thing in 1936/37 and in 1947/48. Each time the bond market called it better.

The reason they were slow to react when inflation actually did appear in 1965 was because they were trigger-shy, having been overzealous many times before!

When you consider the mistakes the Fed has made in the past (and I didn’t even mention Greenspan’s mistakes here), isn’t it fair to say Jerome Powell has handled things pretty well since at least Q1 of 2019?

Powell navigated the Covid crisis admirably.

And he has consistently ignored the pundits calling for a rate hike.

As demand shows signs of not being as strong as first thought, that might prove to have been a very good call.

By comparison, imagine if a pundit like Mohammed El-Erian had been in the seat.

I’m guessing we would have had a couple of recessions already!

Shouldn’t he come with a health warning?

The bond market knows best

Time and again, the bond market has turned out to be more prescient than Fed officials or talking pundits.

The bond market is currently telling us that we should be more worried about growth than inflation.

That makes sense.

Growth in China and the US is faltering as evidenced by the recent GDP prints in both countries.

It is not the end of the world if demand is not as strong as we thought.

High prices are often the best cure for inflation. Demand eases when prices are high.

And there are other levers to help us stave off deflation, notably public spending and structural reform.

Japan got out of its funk when there was a combined effort of public spending, monetary easing and structural reform.

But it does perhaps help us put the “inflation/Zero Hedge” crowd in a box.

And it makes people like Jack Dorsey seem childish with their calls for “hyperinflation.”

Positioning?

As discussed previously, equity markets should be robust into January.

The tapering mid week is having the same effect it has done over the last 12 years.

Bond curve flattens.

Inflation expectations roll over.

Growth stocks go up.

In short, it is a non-event.

The earnings season has been very good thus far.

Even when companies didn’t forecast as high as the street, the market kept buying (HUBS, PAYCOM).

I continue to see no reason to own material stocks, even though some are starting to look oversold.

China slowing down in 2012 was not positive for Vale in Brazil.

It won’t be now.

Value vs Growth

There are some relatively cheap “value” names currently but I do not see a massive mean reversion trade.

I don’t see why value should make a resurgence relative to growth.

I think it will pay to stick with high and sustainable revenue growth companies, which have the potential to expand margins. SaaS?

To stave off higher corporate taxes, can’t the tech compounders just invest in their businesses by way of spending on capital investment, increasing depreciation expense and shielding some pre-tax income?

If you add the potential of buybacks, I see no need to worry about positions in Apple and Microsoft.

And don’t higher corporate taxes mean companies with high dividend payout ratios will have less after tax free cash flow to pay shareholders?

There are some “value” names that could turn into massive growth stocks overnight like Nintendo but you might as well wait for the news of a change in strategy.

In the meantime, stick with the tech compounders and SaaS plays in the US.

The BoE Didn’t Raise Rates - perhaps they never will

The BoE followed Australia and the US and didn’t raise rates.

My guess is rates are going to be at these levels for a VERY long time.

In fact, at some point, I think they will go negative in the US like in Europe and Japan.

The banks are not just playing game and lending enough. Didn’t that happen in Japan in the 1990s?

What is wrong with banks?

Isn’t it time for bank reform?

No amount of UX on some venture-backed neo-bank app can make the app solve the big issues.

Only banking reform can solve the problems or negative rates.

Discount rates and cash flow

If the discount rate is low, what will that do to valuations for high free cash flow yield, tech compounders?

If mortgage rates are low, what does that mean for homebuilders/property developers, especially when there is a shortage of housing?

If corporate debt payments are low, what does that mean for IT spend in an age of digitalization?

What does it mean for buybacks? Why would a corporate pay 2-3% dividends when they can buy back stock at 50 bps?

Should these questions guide investment decisions? I personally think so.

The Old Natural Tech Monopolies Are Making a Comeback

The late 1970s/early 1980s was a special time.

It was a moment in time when many great tech companies were founded.

Companies like Microsoft, Apple, Oracle, Cisco and Qualcomm went on to develop a formidable position in their respective verticals.

Microsoft and Apple get a lot of attention but it’s easy to miss how well positioned the other three might be for the next 10 years.

Qualcomm had amazing earnings! It will dominate 5G and will have years of growth now.

Oracle is the only major public cloud hyper scaler that also has an enterprise database with 40% share, ERP/CRM apps and data management platform.

Larry is a smart man and knows there’s still time to become even wealthier.

And Cisco might just have its own Microsoft moment at some point.

The current CEO reminds me of Steve Balmer.

He is, at his core, a sales guy, who might not get the credit of doing all the things that will ultimately lead to the rebirth of the company.

When people talk about retirement, I think a healthy allocation to such names might make more sense for people than bitcoin.

Perhaps I’m wrong.

As always, thanks for reading. If you like what you read, please share it with friends, colleagues and family. I am still in the building phase. As always, feel free to send me feedback. I can handle abuse.

DISCLAIMER: None of this is financial advice. The opinions expressed are purely my own opinions and it is imperative for you to do your own research. They do not represent the views of any company I am associated with.