The Week That Matters (27 Nov-1 Dec, 2023)

The Week That Matters (27 Nov-1 Dec, 2023)

"You're the measure of my dreams" Shane MacGowan (RIP)

Pivot?

Bill Ackman must be a reader of this newsletter. The author has argued that “higher for longer” was mere rhetoric from neoliberal hacks. They have held on to the notion that Volcker’s playbook from the 1970s can be applied to today’s economy. It can’t. COVID was a once-in-one-hundred year event. Inflation was always going to be transitory. The world’s issue is deflation and low growth. It’s been that way since at least 2008.

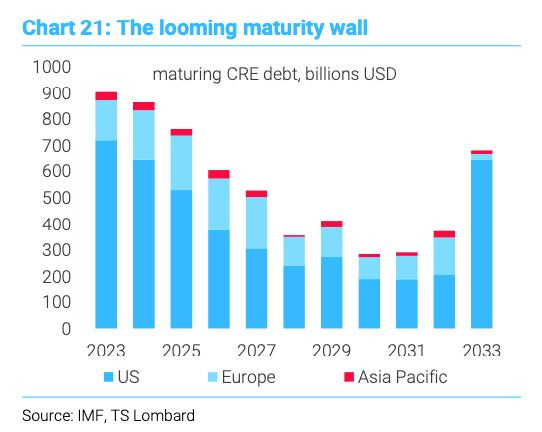

Ackman is right. A financial crisis might be needed for the Fed to change course meaningfully. And it’s clearly possible that one might be around the corner as Powell has embraced Volcker’s approach of going way too far. Financial conditions are excessively tight. But the author doesn’t necessarily believe the real estate sector is as vulnerable as we think. Take a look at this chart:

Maturing CRE debt in the US reached a peak in 2023 and its growth will be declining until 2028. At the same time, long and short term yields have also peaked and are heading south. As discussed before, every one of the real estate professionals in the US the author knows refinanced just before COVID. The terms were too good.

And to be fair, we must remember Powell is not Paul Volcker. Volcker was as every bit as arrogant as Larry Summers is today whereas Powell comes across as someone who is not sure of himself. He knows he is not on the same level as a Janet Yellen, an Alan Greenspan or a Ben Bernanke. This means he will be much more malleable if the winds change shift as they are doing now. He will be cooperative with The White House whereas Ronald Reagan couldn’t stand Volcker.

Encouragingly, there are signs that people within the Fed are starting to pay attention to real time data at long last. The Cleveland Fed is now looking at something called “new tenant rents.” That’s a step forward. It means the Fed might actually start paying attention to what is actually happening with rents, not what happened 12 months ago.

The fact that this hasn’t been done before is an issue in itself. We live in an era of real time data. For rents, we already have the Zillow Observed Rent Index (ZORI), which has been markedly lower than government numbers for a while now. As rent represents such a big chunk of the CPI composite, will we soon see CPI fall off a cliff? The author thinks so. It might fall fast enough to force Powell to do something without the need for a crisis. Let us hope.

Play for the Recovery?

The author has argued that everything we are seeing is NORMAL. The volatility we saw in the late summer (Northern Hemisphere) was to be expected in the third year of an election cycle as is the move higher now in equity markets. There is every reason to believe buoyant markets will continue until the end of Q1 2024 at least.

Paul Krugman wrote a brilliant piece recently asking why economists have been so wrong, especially about inflation. The author would suggest it’s an accusation that can be leveled at famous fund managers and the countless bearish newsletter writers out there.

The internet means that everything tends to be documented and most stuff is reasonably accessible if you look hard enough. This means it’s easy to see what a Stanley Druckenmiller or a Howard Marks was saying in 2010-2012. If you do bother to look, you will see it’s more or less what they’re saying now. They demonstrate an intellectual laziness that might come with age or just with having lots of money. The author is not sure. But it’s the author’s opinion that they will be proved wrong AGAIN.

In the 1990s, Greenspan cut three times consecutively, which led to the longest economic boom ever seen during the Clinton years. The three-cut series was the “magic sauce in the 1990s to get growth to stop slowing,” as the great Ed Hyman noted.

It’s time to think through what lower interest rates would mean for large cap technology stocks (will Apple and Microsoft be USD$10 trillion companies in this cycle?) and what they will mean for IT capex and the like. Digitalization was a much discussed theme a couple of years ago. The higher interest rates have obviously impacted investment in that area but what happens when cash flows spike thanks to lower costs of capital?

We also live in a Victorian Age of technology. A few companies are impacting our lives in ever increasing ways and there is some evidence that Silicon Valley has managed to do what it said it would: create category killers that have enough scale to compound returns for years to come. Uber?

And we are on the cusp of the monetization of AI. Microsoft lead the way with the benchmark pricing it announced in September. Its subsequent moves with Open AI make the author feel he got it right. It will be the large tech companies that lead the AI narrative, not Silicon Valley. Any good tech will be sucked into the likes of Microsoft, Salesforce or Apple. The trick is to find private AI businesses with the 4Ps:

Proprietary Technology

Patented Technology

Product Market Fit

Positioning (ability to scale)

The M&A bonanza is about to start and the author believes it will last for 24 months.

Private SaaS Valuations

Where Salesforce goes, lesser SaaS plays follow. The numbers from Salesforce were great this week, as always, and this should remind everyone how accretive a successful SaaS business can be. And of course, in a falling interest rate environment, sticky, consistent revenue is king, no?

The author is starting to see Venture Capital firms invest again. The author believes there will be a frenzy of investment in the 1st and 2nd quarter of next year. As argued before, venture capital is still an inverse beta play on interest rates for the author. And the professionals who run these firms have been too cautious over the last couple of years and need to act soon or they will return little, if any capital, to their investors.

One positive might be a thawing of the IPO market. It has been in the doldrums for a while now. The peak coincided, interestingly, with Bill Gurley arguing that direct listings made much more sense than the traditional process of listing companies. It was the height of hubris for the Valley.

Importantly, Figure, the blockchain start-up, announced last week it was working with Goldman Sachs, JP Morgan and Jeffries on a potential IPO of its lending arm in early 2024. Bloomberg reported it was looking for a valuation of $2-3 billion. It might hit the market at the right time and might drive private tech valuations higher.

Would Charlie Munger have bought Amazon if he had lived?

Charlie Munger saved Warren Buffet at least two times in his professional life. Buffet was a mess when his Senator Father retired from politics and actually looked to disband his partnership. He worried about his edge. It was fortuitous he met someone as brilliant as Charlie. Without him, Warren Buffet might have not been the household name he is today

Charlie also saved Buffet when he forced him to buy Apple. Without Apple, Berkshire Hathaway would have gone the way of General Electric. Its portfolio companies were ok but it needed to invest in Apple to keep up with the market.

It is naturally sad to see Charlie pass. He was a brilliant man and arguably the author’s favorite billionaire, if such a category exists. But it does raise a few questions.

Why has the succession plan been so poor? At 99, Charlie was still very much on the tools apparently as is Warren Buffet today. Was that sensible? KKR, who would have compounded returns, if they could have held on to their investments longer, much more than Berkshire Hathaway, managed a seem less transition with no obvious impact to the business a few years back. Why didn’t Buffet do something similar?

Greg Abel, Charlie’s successor, is an incredibly capable chap. But is he the right guy for Berkshire Hathaway now? Wouldn’t a fund manager from somewhere like Baillie Gifford have been more appropriate for the next 20 years? What if Cathie Wood is correct about some of her assumptions?

The trading companies in Japan are cheap, have good ROE potentially and will serve Berkshire Hathaway with a high volume of deal flow but they will not necessarily compound like a technology stock. If Charlie had lived, what other technology stock would he have bought?

In response to the last question, the author would suggest he might have looked at Amazon.

Historically cheap (EV/Gross Profit 6.4x)

AES, Prime and Ads growing double digit

Online store seems to be a drag but the gross margin dynamics look better.

Thoughts? He could have switched out of his position in Alibaba. (The author has no position in Amazon! Asking for a friend.).

“The ginger lady by my bed.”

Finally, it was sad to hear of Shane MacGowan’s passing. He loved the ginger lady (whiskey) a bit too much but he was easily one of the best wordsmiths in popular music ever and “You’re the measure of my dreams” has to rate as one of its most poignant lines.

As always, thanks for reading. I’m over the Christmas celebrations already (they start early in Oz). Wishing you the best in trading, business and family this week. None of this is financial advice - do your own research!

Best regards

Mateen

DISCLAIMER: None of this is financial advice. The opinions expressed are purely my own opinions and it is imperative for you to do your own research. They do not represent the views of any company I am associated with

"So can anyone" Shane MacGowan

Merry Christmas