The Week That Matters (23-27 Oct, 2023)

The Week That Matters (23-27 Oct, 2023)

“Japan today reminds me of the 1960s and 1970s in the United States.” George R. Roberts, KKR, 2019.

Powell’s pivot might come too late

It’s not wise betting against the market in November and December of any year, especially if that year is the third year of an election cycle. There tends to be a dramatic seasonal effect. One of the only times in recent years the market hasn’t rallied hard into Christmas was in the autumn of 2018 (Northern Hemisphere). Interestingly, that was when Powell made his first big mistake, by taking all the liquidity out of the system as he has done now.

Despite the sloppy tape last week, US earnings weren’t bad. We had beats across the board (only TSLA sucked) and we have Apple next week. Microsoft’s earnings, especially its comments about AI, would have been better received in a more optimistic tape. And people over-reacted to Google’s print, in the author’s opinion.

The earnings out of Japan, however, have been more disappointing by and large. Given it has some of the best machinery and factory automation plays in the world, how those companies think about the future can be a good indicator for global growth. If you listen to the companies, capital expenditure is slowing across the globe, with particular weakness in China and Europe. Declining capital expenditure is never good but it does fit in with this newsletter’s general thesis.

A growth problem, not an inflation problem

The author has always argued the world has a growth problem, not an inflation problem. We have been growing below trend growth since 2008. At the end of 2019, just a few months before the lockdowns, central banks were pulling their hair out. Everything seemed incredibly deflationary - low growth, low interest rates, low inflation.

COVID took our attention away from the underlying issue but COVID was a once-in-one-hundred year event. It caused havoc to supply chains like the German U-Boats did with US food supplies to Great Britain in 1917 but the impact was always going to pass. And the re-shoring we have seen (de-globalization) was never going to be as inflationary as first feared.

Powell MUST pivot soon or he will cause a financial crisis. Inflation is in the rear-view mirror now. His higher for longer stance is just not compatible with declining inflation and lower nominal growth. History looks back on Paul Volcker positively because the Friedman faction wrote the history books. Paul Volcker was not, however, what they say he was. He caused two unnecessarily severe recessions in the early 1980s. (That’s why Ronald Reagan hated him). If Powell causes a financial crisis, it’s doubtful people in years to come will remember him so fondly.

Two Misleading Economic Narratives

The author struggles with narratives that have little substance but become broadly accepted tropes. As Edward Bernays, the self proclaimed “father of public relations,” noted:

“We are governed, our minds are molded, our tastes formed, our ideas suggested, largely by men we have never heard of.”

Isn’t that why you should turn off the TV sometimes if you want to make long term investment decisions? Let the author pick two examples:

“Higher yields are doing the Fed’s job for them”

Really? Is that how it works? Higher yields imply to the author, at least, that financial conditions are just too tight. That’s it.

Higher yields add to the inflation issue. It doesn’t solve it. If you have three buy-to-let properties in London and the interest rate on the mortgages goes up, do you raise rents or lower them as a landlord?

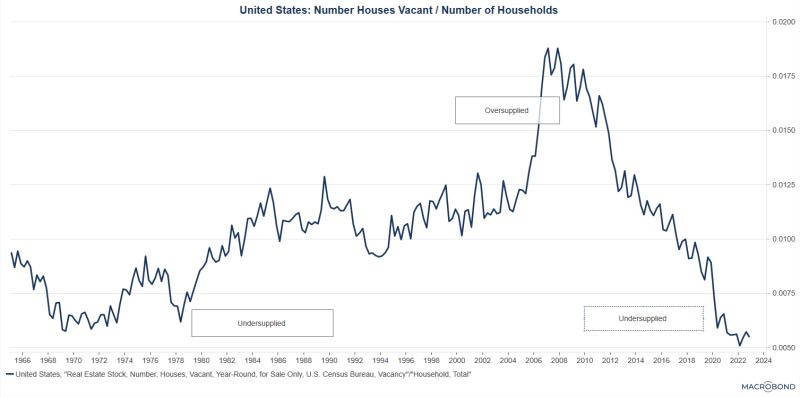

Also, don’t higher rates stifle investment in productive capacity? The chart below illustrates how bad the housing crisis is:

What do you think happens to housing supply if rates stay where they are? We need lower rates so companies like Lennar can do what they’re good at, no?

The truth is the Fed doesn’t have many tools in its arsenal. And it shouldn’t raise the rates the way it has EVER. It’s simply too dangerous. All it has done is crush the working poor and the indebted middle class. It also creates a very real risk of a blow up somewhere in the system.

It does nothing, however, to solve the structural issues (industry concentration) that clearly exist in areas like healthcare that create ever increasing prices for consumers. For that, you need courageous politicians, who are ready to take on the lobbyists. Unfortunately, courageous politicians are in short supply everywhere.

“US Treasuries are going to lose their safe haven status”

Even Mohammed El-Erian joined the bandwagon this week. That was somewhat disappointing as what exactly is the alternative? Gold? The Euro? Bitcoin? You have to be joking!

It’s not surprising that we have got to this, to be fair. Powell is causing havoc to the financial system. US politics is in dire straights. People are freaking out about deficits (unnecessarily in the author’s opinion). And even Janet Yellen argued last week that the US can fight two wars!

Incidentally, what is happening to Janet Yellen btw? She was solid in the Fed and she was one of the best Treasury Secretaries the US has had (maybe Steve Mnuchin was better!). She has to return to thinking about employment, infrastructure spend and education. She is awesome but seems to be increasingly pulled into politics. But the author digresses.

Concerns about US treasuries will pass. The US is not Argentina. It is not Weimar. Given what is happening in the world, it is only becoming stronger. Europe suffers from the War in the Ukraine. The US, by and large, benefits.

Conversations around public deficits also never take into account income. What will the GDP be of the US, especially if it gets its energy policy right, by 2040? Doesn’t that kind of matter too?

Finally, can we really fathom the wealth of the US? Only Japan and maybe China come close and they are a very distant second or third. Think universities, IP, infrastructure, people. Their corporations win most commercial battles (Apple, Microsoft) and their military has no competition (US has 12 aircraft carriers; China has 1?).

Those things matter. We spend a lot of time hearing about Norway’s sovereign wealth fund but what would the size of the US sovereign wealth fund be if they had one?

Markets

The author mentioned the autumn of 2018 earlier. That was when Powell tightened too aggressively. Interestingly, that caused a spike in real interest rates too. Importantly, when they started declining in December 2018, the equity markets stopped throwing a tantrum and started turning up.

It is this newsletter’s contention that real interest rates, which have been going up to the right since late December 2021, might be rolling over finally. That is significant as it will ultimately be supportive for equity valuations.

Last week, we even saw the Magnificent 7 get hit as a group. They have held up well and fund managers probably wanted to take some risk of the table. But how long will that last if real interest rates come off now? In a declining real interest rate environment, high ROIC stocks tend to do quite well, no?

It must be said, too, that a lot of charts (non-Magnificent 7) are near October 2022 levels. The Russell 2000 actually is below them. Last week some of those stocks started to look more constructive. Outside of the Magnificent 7, has the recession been priced in?

It isn’t easy right now and the author has very little exposure. A lot will depend on the messaging from Powell this week. We need a communication pivot first. Unfortunately, Christine Lagarde in the ECB didn’t give us enough last week to signify that will happen, despite lending data in Europe in September looking like it’s falling off a cliff. One can only hope at this stage.

“Japan today reminds me of the 1960s and 1970s in the United States.” George R. Roberts, KKR, 2019.

There is a long history in Japan of foreign activists and PE firms trying to unlock value in Japanese corporates. Way back in the late 1980s, American corporate takeover specialist, T Boone Pickens, tried to unlock value in a Toyota subsidiary, Koito Manufacturing, and failed. The Japanese press often described him as an example of a “Barbarian at the Gate.” (The book about the LBO of RJR Nabisco had just been published). More recently, in 2013, Daniel Loeb’s Third Point tried to force an issue with Sony but failed to get them over the line, although Loeb wrote a couple of now famous letters to the company.

Japanese corporates, for their part, have naturally worried about the intentions of these foreigners. Is that really that different from US or Australian corporates? The Yanks didn’t like the British corporate takeover specialist, Sir Jimmy Goldsmith, in their backyard in the late 1960s. The Aussies have been wary about Chinese and Indian influence here.

And to be fair, Japanese activists had little impact either. And one famous fund manager, Yoshiaki Murakami, didn’t just get push back. He actually ended up in prison!

But things are changing in Japan in material ways. Conglomerates would traditionally prioritize size or employment or stability over shareholder returns, and they wouldn’t sell off struggling divisions. That attitude has slowly been changing due to top down reform.

One of the best examples of the change that is taking place in Japan is the split up of Toshiba in 2021. One of the oldest and most celebrated global brands in Japan getting under the hood and recalibrating its growth engines made headlines. It was a significant event, similar to when Hewlett Packard broke away from HPE in 2015.

Interestingly, KKR has just pulled off what many PE firms have tried -- and failed -- to do in Japan for decades. It acquired a neglected division of a Japanese conglomerate, overhauled operations and then took the company public for what looks like a sizeable return.

KKR bought what is now Kokusai Electric from Hitachi in 2018 and gave management significant incentives to boost performance at an overlooked business. Kokusai started trading on October 24th in the biggest IPO since 2018. Shares jumped as much as 29%.

This is a significant event and is yet another reason to look at Japanese equities with fresh eyes. The focus this week will be on the BOJ but it’s at a corporate level that things are getting very interesting indeed.

As always, thanks for reading. I am on the road with the oldest venture debt fund in Silicon Valley this week seeing Australian investors. (I hope to see many of you at the meetings or lunches). I wish you the very best with trading (it’s really hard at the moment!), business and family this week.

Best regards

Mateen

DISCLAIMER: None of this is financial advice. The opinions expressed are purely my own opinions and it is imperative for you to do your own research. They do not represent the views of any company I am associated with.

Thc always a good read