The Week That Matters (13th-17th Nov, 2023)

The Week That Matters (13th-17th Nov, 2023)

"Financial markets (speculation) are really the force by which we move capital to its best and highest use" Kenneth C. Griffin, Citadel

Sohn Hearts and Minds Conference - It felt like 2009!

The author was lucky to get a ticket to the Sohn Hearts and Minds Conference in Sydney last week (thanks again, S!). Although he spends a great deal of time working with private tech companies, he loves public markets and tends to enjoy a good stock pitch over one from a start-up.

The pitches were great, to be fair. The author’s personal favorite was the one for NexGen Energy by Terra Capital. This newsletter is a massive bull on uranium and so the fund manager was preaching to the converted. The author bought some more of the stock on Friday night.

Separately, it was great to hear directly from Dan Loeb of Third Point. The author has a copy of the letter he wrote to Sony in 2013 in his notes (the author clearly needs more hobbies) and is a big fan. Although Dan had a lot of great things to say, it was somewhat disappointing to hear he was launching a new credit fund. (Does the world need another one?) More importantly, though, he made an interesting point about companies deleveraging over the last couple of years. Isn’t that another reason to be bullish when rates come down?

Cathie Wood didn’t disappoint. Her star is set to rise again, as we fast approach a pre-Covid environment - low growth, low interest rates, low inflation. Her optimism on self-driving taxis seems extreme but her general view that we live in a Victorian Age of technology, where numerous tech verticals converge, makes perfect sense to the author. This newsletter bought more of ARKK ETF on Friday following her speech. For the author, the Robinhood brigade will view it as the NASDAQ of the 1990s soon enough. NASDAQ is too blue chip today to get the big moves.

It wasn’t all positive, though. The author was surprised by some of the narratives given by the fund managers, who didn’t pitch. They all kind of said the same thing. They were positioned cautiously with one famous firm even advising investors to hold cash! (Yawn!) None of them seemed positioned well for a fall in interest rates. None of them was overweight growth names.

It felt, in this regard, very much like what the conference would have been like in January/February 2009. At that point, no one believed in a recovery. At that point, people like Stanley Druckenmiller were claiming equities would experience a lost decade as he suggested at the lows in October 2022 and more recently, at the potential lows of October 2023. Timing’s a bitch?

Perhaps the most amazing statements the author heard was “growth was uncertain,” and “there are numerous potential outcomes.” The author remembers hearing exactly the same thing at the start of the post-GFC rally. And from an intellectual point of view, isn’t growth always uncertain and aren’t there always a myriad of potential outcomes for an investment? Maybe the author is missing something.

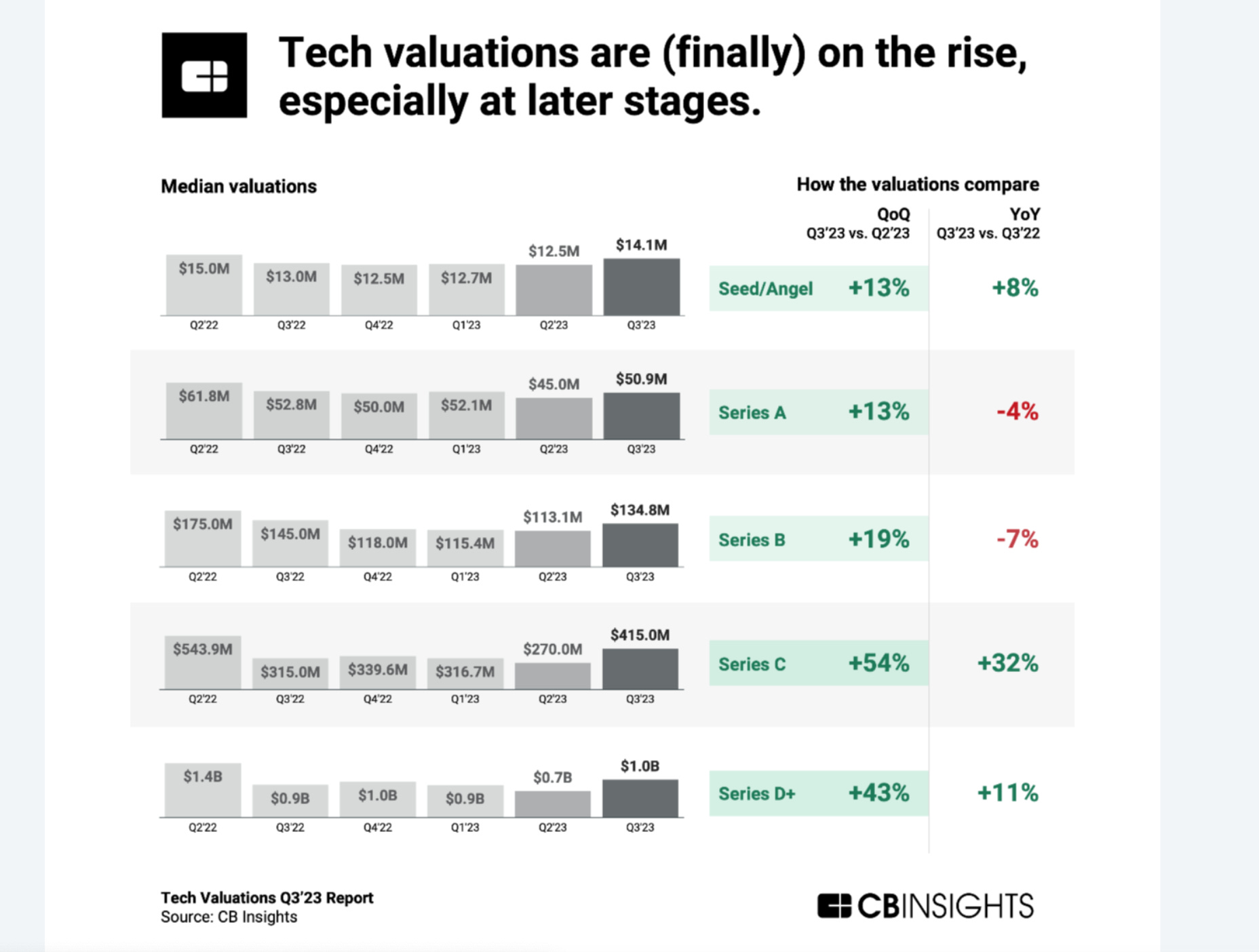

The author came away feeling more bullish than ever. If Powell does cut 100 bps in January, he thinks the big money isn’t positioned well. He would even suggest the investment world is OVERWEIGHT private credit and UNDERWEIGHT listed tech.

At times like this, it’s always important to remember that George Soros and David Tepper made a lot more money playing the recovery (2009-2012) than Michael Burry ever did shorting housing. The Lesson: Be like Tepper!

Incoming Speculative Market?

The author remains optimistic but part of him thinks things could even start to get silly soon. There are plenty of signs that risk appetite is returning aggressively. EtherRock NFTs and Bitcoin Rock Ordinals are selling for over $100,000 again. Biotech stocks are perky. And VC valuations are increasing.

The author has no interest in taking excessive risk (he is old and likes to sleep at night) and there might be enough valuation uplift in many large cap, listed names in the US anyway.

That being said, he thinks it’s time to think through more earnestly what happens around the world if US rates do fall aggressively. EM including China should catch a bid, but the author would suggest it should also be very positive for Japan.

The Bank of Japan has probably been pulling out its hair looking at the interest rate differentials driven by Powell embracing the ghost of Volcker. Once Powell starts cutting, the Yen should look positively cheap, as Japan normalizes its interest rate policy. What does that do interest in the Nikkei, which has seriously underperformed the S&P500 in USD?

He also strongly believes that if rates fall in the US, it will be a bonanza for alternative asset fund managers. This is the time to look at great fund managers from around the world. The author is obviously talking up his own book here!

AI will lead?

The author has little interest in Sam Altman’s travails at Open Ai. If he has lied to the board, it’s a win for corporate governance. If it’s a move by Microsoft to take over the company, it’s a positive. Sam is smart but Nadella is the GOAT. If it’s about the family matter, it makes sense for him to go. It sounds horrible.

Much more important is the acquisition by AirBnB of Gameplanner.Ai for $200 million. The author believes we will soon see a frenzy in M&A in Ai private businesses. Silicon Valley will not control the narrative of Ai. Large cap tech will be the main driving force for what happens.

A lot of businesses out there claiming to be an AI business are nothing of the sort. The author suggests using the 4P’s to identify good opportunities. It will narrow down your search:

Proprietary Tech

Patented Tech

Product Market Fit

Positioning (ability to scale).

As always, thanks for reading. It’s a short one this week as it’s a mad rush until the end of the year. The Aussies do holidays as well as the French do and soon enough, it will be doors closed for the year. Wishing you the best with family, business and trading this week. None of this is financial advice. Do your own research!

Best regards

Mateen

DISCLAIMER: None of this is financial advice. The opinions expressed are purely my own opinions and it is imperative for you to do your own research. They do not represent the views of any company I am associated with